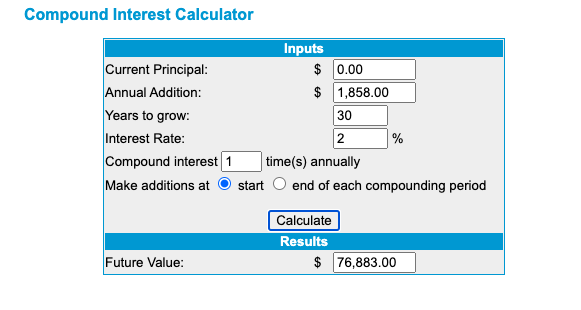

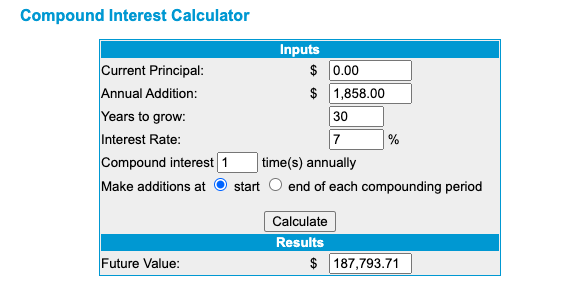

Photo Credit: Michael Longmire and Unsplash According to an article I came across today from USA Today the average household only saves about 7.5% of their income. This was eye-opening to me. Personally, I'm saving about 30% of my income between a high-interest online savings account, a SEP-IRA and a Roth IRA. To see more click on this article. In this process I'm not giving up many of the luxuries in my life such as travel, going out to eat and my gym. I'm simply cutting out many of the expenses that I don't really care about such as buying a new car every 3-4 years or buying new clothes constantly. Let's say your household takes in the average household income of $61,937. After a 20% deduction for taxes and benefits you are bringing in a net of $49,546. If your household saved the average of 7.5% they would only be putting roughly $3,716 annually into their savings and investment accounts. We'll split this income evenly into a high-interest savings account (say a 2% annual interest rate) and buying a traditional index fund with a 7% annual growth rate. What would we have after 30 years? High-Interest Savings Investment Account Would This Be Enough to Live on?The short answer is no using the 4% rule made popular by the FIRE movement. Not unless you believe you can live on about $10,000/year in the year 2055. Also you should be crossing your fingers that Social Security will still be there when you hit the eligibility age.

The answer to this is either playing more offense or more defense. Just like any good sports team there is a level of synergy between the offense and defense that create optimal outcomes. You should think the same way with your money. Playing better offense means finding ways to grow your money through investments or simply increase your income. I'm a bigger fan of this route, because you're probably worth more than what you give yourself credit. You could take on a side-hustle, ask for a raise or change jobs. Playing defense means creating a budget, cutting out things you don't need and saving more money overall. This could mean going out to eat 2x a week instead of 5x or shopping for clothes in a 2nd hand store instead of high-end stores. The little changes add up over time. Only saving 7.5% is pathetic and keeps you on the wheel like a hamster going nowhere. The only excuse for only saving 7.5% of your income is because you're paying off debts such as student loans, an affordable mortgage, credit cards or medical bills. Saving 15% should be your absolute minimum goal. You should enjoy the ride to retirement, but have no worries once you get there.

0 Comments

Leave a Reply. |

Archives

September 2020

Categories

All

About the AuthorAndy Rupert is a Penn State (B.A. John Curley Center for Sports Journalism 08') and a Southern Miss (M.S. Sport Management 09'). He has spent his whole career working in sports and tourism digital marketing and metrics. |

RSS Feed

RSS Feed