I found myself making a comfortable lunch today that was quick and easy. Once I was done and sitting down at my coffee table I had to laugh. Why, you ask? I bet anyone I'm related to can tell you without reading any further. You see growing up in a family of six in rural Pennsylvania traveling that involved hotels wasn't the most cost effective way to see the world. My family had a pop-up camper that allowed us all to stay together at campgrounds for a reasonable price. Many of our meals comprised of a peanut butter sandwich (or just a slice of bread with peanut butter on it) with a piece of fruit and more than likely a Little Debbie. In our family, the Oatmeal Cream Pie held a special place. But heaven forbid you open it up before the other items were gone. When we traveled Mom was very persistent that we have to finish our sandwich and fruit before you can have the Oatmeal Cream Pie. Depending on how dry the bread was or overly ripe the fruit may have been might have been a difficult task for most 7-18 year olds. For a plate you tore off a paper towel, found a picnic table at a rest area and ate your meal before we got back on the road to continue the journey. Buying food for six people at a Wendy's or McDonald's not only wasn't nutrient rich, but also was expensive. In her mind she might have viewed this simply as feeding her kids without wasting time and money. To me looking back on it, it was a lesson in those things and delayed gratification. How does this relate to the world I see when I step outside my door? So many people just want to fill themselves with the dessert without putting in the work of getting the vitamins and nutrients of the rest of the meal. Their entire lives are living for the short-term. They want to be physically fit using some diet pill instead of simply burning more calories than they consume every day. People expect a high paying job without the hard work of building a strong body of work. This is why people invest in get rich quick schemes or waste their money buying lottery tickets rather than contributing money to investments and investing in assets. What are you willing to sacrifice today to get to the rewards of tomorrow? Can you give up going through the drive-through every morning? Something I am sure your waistline and wallet would both thank you for. Can you give up buying a new truck every 3-4 years and ride it out with one for 10-12 years so you can invest money through index funds or open a Roth IRA? Your 65 year old self will thank your 35 year old self. Can you give up an hour of Netflix or Hulu every night to build skills that get you where you want to go? The next time you have a job interview you'll be well-rounded by some new skill that allows you to add value to their business. Can you give up happy hours and drag your butt to the gym every evening? You'll sleep better, feel better and have more energy. Can you pass up the sweet snacks throughout the day in favor of fruits and vegetables? You won't just get a bunch of hollow calories. Can you not open Facebook or Instagram to get your news, but rather sit down with a book on history? You'll become a more well-rounded individual in conversations. There are entirely too many people out of shape, living in debt and without skills that are too weak of will to say "no". How has this lesson impacted my current life? I'd say there are many ways that this has benefitted me. Anyone that spends time with me can be annoyed by my love of lists and routine.

Many of these tasks call for a lot of short-term sacrifice and saying "no" to friends and family. Sometimes saying "no" is easier than other times. However, staying disciplined to my goals above has allowed me to stay healthy, fit, well insulated from financial hardship, mentally happy and well educated in a variety of disciplines and view points. If you're into delayed gratification enjoy one of behavioral economics favorite experiments. The marshmallow experiment for kids. I would be willing to bet that there are some adults that couldn't pass this test.

2 Comments

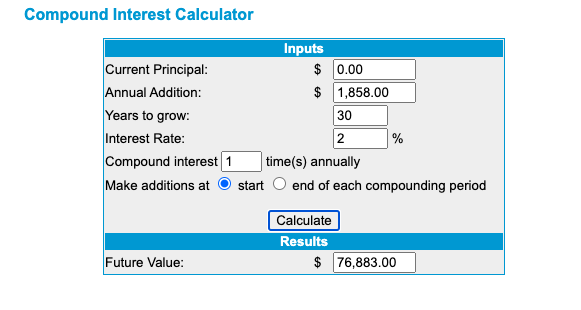

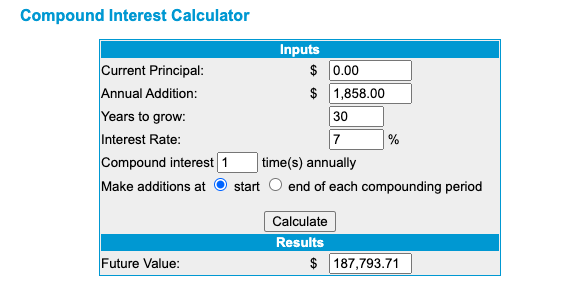

Photo Credit: Michael Longmire and Unsplash According to an article I came across today from USA Today the average household only saves about 7.5% of their income. This was eye-opening to me. Personally, I'm saving about 30% of my income between a high-interest online savings account, a SEP-IRA and a Roth IRA. To see more click on this article. In this process I'm not giving up many of the luxuries in my life such as travel, going out to eat and my gym. I'm simply cutting out many of the expenses that I don't really care about such as buying a new car every 3-4 years or buying new clothes constantly. Let's say your household takes in the average household income of $61,937. After a 20% deduction for taxes and benefits you are bringing in a net of $49,546. If your household saved the average of 7.5% they would only be putting roughly $3,716 annually into their savings and investment accounts. We'll split this income evenly into a high-interest savings account (say a 2% annual interest rate) and buying a traditional index fund with a 7% annual growth rate. What would we have after 30 years? High-Interest Savings Investment Account Would This Be Enough to Live on?The short answer is no using the 4% rule made popular by the FIRE movement. Not unless you believe you can live on about $10,000/year in the year 2055. Also you should be crossing your fingers that Social Security will still be there when you hit the eligibility age.

The answer to this is either playing more offense or more defense. Just like any good sports team there is a level of synergy between the offense and defense that create optimal outcomes. You should think the same way with your money. Playing better offense means finding ways to grow your money through investments or simply increase your income. I'm a bigger fan of this route, because you're probably worth more than what you give yourself credit. You could take on a side-hustle, ask for a raise or change jobs. Playing defense means creating a budget, cutting out things you don't need and saving more money overall. This could mean going out to eat 2x a week instead of 5x or shopping for clothes in a 2nd hand store instead of high-end stores. The little changes add up over time. Only saving 7.5% is pathetic and keeps you on the wheel like a hamster going nowhere. The only excuse for only saving 7.5% of your income is because you're paying off debts such as student loans, an affordable mortgage, credit cards or medical bills. Saving 15% should be your absolute minimum goal. You should enjoy the ride to retirement, but have no worries once you get there.  Photo Credit: Ian Baldwin and Unsplash Needless to say 2020 has not been kind to the folks that work in hospitality, live events and tourism. I've spent my entire career in this niche. Tourism is really fed by hoards of people coming to town for major events and conferences. They don't come because they enjoy the local Holiday Inn Express or Super 8, they're there because something is going on that creates the necessity for an overnight stay. Restaurants depend on both locals and visitors coming to their restaurants with consistency. Live events, namely concerts, festivals and sports depend on their turnstiles for their revenue. If they're interesting enough, they might create some TV or online viewership revenue. However, these industries are battered and bruised right now, even as you see other industries essentially go untouched or even thrive in the current conditions. We have no idea when the hard news will let up. Those that haven't largely been impacted financially have a responsibility to help thy neighbor.  Photo Credit: Rabia Jacobs at Unsplash Shop and Eat LocalWhenever you pull through the drive-through of McDonalds, hit the buy button on Amazon or pick up a few groceries at Wal-Mart you aren't helping your local economy. Sure, they might pay some people enough to barely get by and pay their local taxes, but the bulk of their revenue is going elsewhere. You should look to eat at non-chain stores that are locally owned, employ local people and keep their money in their community. Figures that I've heard from a variety of studies is 55%-80% of revenue stays local when you shop local, while 8%-15% stays local when you shop at a major chain store. The publicly traded major chains can shoulder the swings and the smartest communities limit their entry to the market to begin with. If you're a big proponent of "Made in the USA" do it one better. Drive by Target and Wal-Mart and put your money where your mouth is and buy local. Buy Gift CertificatesRestaurants and locally owned stores need revenue now to cover rent, utilities and whatever staff they have left. They are frustrated by wild swings in occupancy limits and regulations sometimes with little or no runway to implement them. Just because a store's capabilities are limited doesn't mean the bills stop coming in the mail. If you love that restaurant or store because you can walk in and shake the owner's hand support it today. Don't wait until "things get better." Personally, I might go to a chain restaurant once every other week, but 80%+ of my restaurant spend stays in the local community. I love going to farmer's markets and small stores to see what kind of neat items they have. You aren't seven people removed from the maker of the good, but often chatting with them in person. You also get a feel for your destination in a way that a major chain's sterile environment won't ever give you. Buy Merchandise from Local Sports TeamsMinor league sports and small universities are struggling mightily right now. Teams are getting cut, spectators are being left on the outside and some minor league baseball teams are never coming back. You might not be able to attend their games and they might not have a TV deal, but buy some mechandise from their websites. Not Amazon or Dick's Sporting Goods, but their own in-house websites. Also, if you can lock in future season ticket packages or voucher books do so. Buy gift cards that can be used in the park at a future date. If you care to see those teams remain a part of your community in the future, support them today.  Photo Credit: Laura Pluth and Unsplash Take a Driving TripWhen I say take a trip it is quite possible to go for a 3-4 hour drive somewhere and not encounter large crowds. Book a room or a campsite at a new location you've wanted to visit or an old favorite. If you're worried about leaving the state, then don't. There is plenty to explore in your own back yard. Go to stores and restaurants that you can't go to at home (read: Olive Garden and Cracker Barrel) to get a unique experience. Give those businesses positive reviews online. The hotel industry is absolutely cratered right now and you can have your own private room and bathroom on any trip you're on. You probably won't get any better prices and ability to opt-out of a trip than you do right now. But.......  Photo Credit: Julian Wan and Unsplash Wear Your MaskThis is simple. Wear your mask and avoid crowds as much as you can. Anyone can do it. What's the risk-reward to borrow from Machiavelli's "The Prince"? The potential reward is saving hundreds of thousands of lives and the sanity of the healthcare community with the risk of wearing a piece of fabric and avoiding hanging out in crowds. It's not hard. The risk of the inconvenience is well worth the potential reward.

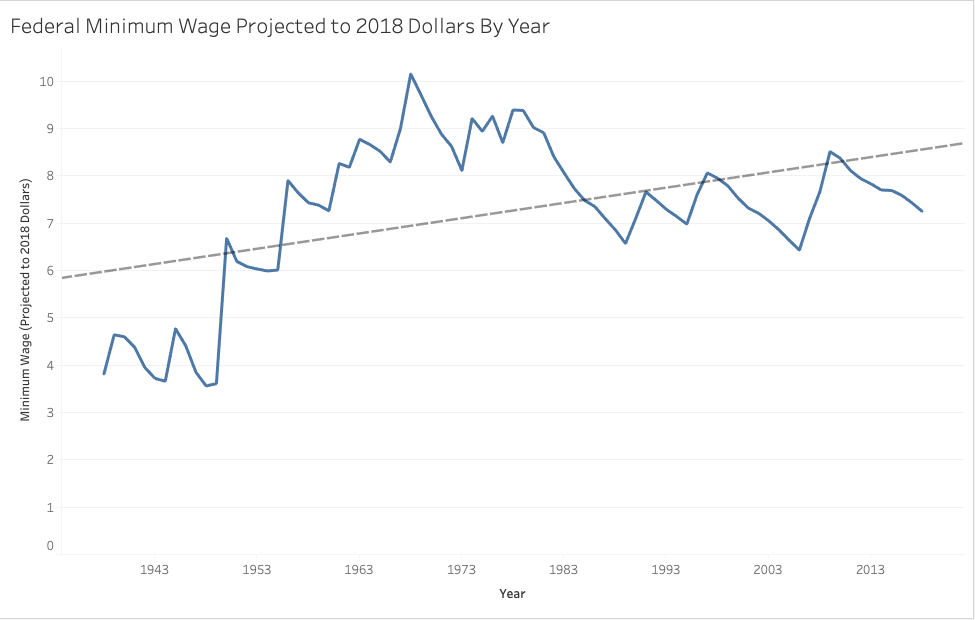

According to CNBC, in 1987 tuition at a four-year public university cost about $3,190/year in 2017 dollars. I created a chart above using Tableau to track the whole history of minimum wage since FDR's New Deal. In 1987, you could pay off your tuition on a minimum wage job in about 449 hours, before taxes. That is 8.6 hours per week. A four-year public university in 2017 costs about $9,970/year. According to the chart below it would take 1,375 hours, before taxes. That is roughly 26 hours per week. The trend line, which creates a fair historical baseline looking at the full history, says the current national minimum wage should be around $9.00. This is well below the $15 that some people are seeking, but we also do have to consider this is a national number. Midtown Manhattan isn't the same place as rural West Virginia when it comes to how far you can stretch a dollar. In fact, only three years (1997, 2009, 2010) fall above the trend line in my lifetime. If minimum wage got bumped to that it would eliminate about 200/hours of work per year for a college student trying to pay their way through. With numbers like these it is no wonder why many students opt to think long-term and pad their resume for a career rather than working a regular low-paying job. It comes down to simple risk vs. reward. To see the source of the data that I got online adjusted by year, click on the file below.

I've always really enjoyed personal finance and taking lessons from the books I read. One of the first people that got me interested in personal finance was Dave Ramsey. In his book The Total Money Makeover Dave lays out a very clear path on the way to a wealthy and healthy life. Here are Dave's Steps:

There were very few things I disagreed with Dave throughout reading this book on. The two big ones were 15-year fixed rate mortgages and the concept of not having credit cards. I would say that you can make out on a relationship with a credit card company as long as you pay your balance in total every single month. For me personally, I get about $250-$350 annually in cash back for just living my normal life and never carrying a balance to the next month. Also, I'm more of a believer in a 30-year fixed rate mortgage with an absolute minimum of 20% down payment on the home. I just think this gives you more wiggle-room in case of emergencies and you can always pay well beyond your payment to chip away at your principle. This was an outstanding read and is well done. It provides a road map for even the most clueless of consumers. I really enjoyed how Dave has been getting his steps in front of schools and churches to hit a lot of eyes and hopefully spark smarter consumer budgeting.  What Did I Learn?

This book, first published in 1926, is a classic for those in the personal finance world. The text tells lessons about how to become wealthy, but through a narrative story of a young man approaching a rich older man. The book can be a little hard to follow in its original text, because it is full of a "hast" and "thou" style of writing. Ultimately it gives sound financial advice throughout. It can also be read in less than a few hours for those willing to sacrifice the time. Tackled in the book include home ownership, savings, controlling your expenditures, having your money work for you, guarding yourself from poor investments and much more. This is a really good book for anyone that is just starting their personal finance journey with their first job out of school. Personally, I wish I would have gotten into personal finance more as a 20 year old rather than a 30 year old. Lessons like the ones found in "The Richest Man in Babylon" would probably have made me even more money than I have. The story is more about discipline than anything really.  What Did I Learn?

1. The lessons in this book are a little more fundamental (i.e. save 10% of your income) than what you see in books such as Rich Dad Poor Dad or The Millionaire Next Door. Like I said above the story is better serving for those starting out, but there are some lessons for the veterans of the personal finance world. 2. The book doesn't get into the stock market by any means, but it does talk about the difference between a wise and an un-wise investment. One could take this information and apply it to stocks. 3. Unlike a number of other books this book focuses in on home ownership. This story promotes ownership of a home, where more modern books kind of volleyball that point back-and-forth vs. renting. 4. One of my favorites was the Sixth Cure: Insure for a Future Income. This is where retirement and investment accounts fall into the equation. Like most modern beliefs such as The 4% Rule are examples of this. 5. I learned that what I am doing is not a bad plan. My biggest obstacle would probably be increasing my income level. The important thing to take away is not allowing for lifestyle creep when I do get an increase, which is something everyone should be careful of.  Photo Credit: Josh Appel through Unsplash 1. Buying more house than needed.

In the last 45 years, the average square footage of a home has increased by 1,000 square feet. Yes, you read that correctly. Even as family sizes have shrunk and the storage locker industry has grown, we still have homes getting larger and larger. The average house size is now approaching 3,000 sq. feet. Who on Earth needs a house this size that is not the Brady Bunch? It is smarter to buy for what you need, rather than what impresses the Joneses. 2. Carrying over credit card debt. This is just idiotic. You signed up for a credit card whose sole purpose is to wish and pray that you don't pay them back on time. Much like casinos, the house always wins. If there wasn't more money being created in interest from people carrying over their balance than there is with people cashing in rewards then credit card companies would go out of business. However, they are doing so well that their names are attached to bowl games, stadiums and they have national advertising campaigns. Pay off your card in full every month AND cash in the rewards. You can win in this relationship. I make about $30-$40/month by paying my card in full and cashing in the rewards. 3. Buying a new car as soon as the previous one is paid off. The notion that you should always have a car payment is frankly dumb. The goal should be to get the type of car that best fits your habits and pay as little as possible for it. If you're someone that commutes a long-distance and don't own a camper/boat/trailer/contractor business there is no reason to own a large truck. They have bad gas mileage and are expensive to maintain. There is also no reason to own a luxury automobile. In what scenario in your life will you need to have the difference between a 250 horsepower engine and a 400 horsepower engine? The up-front cost is greater and the service of the car costs more than a more common make and model. Get your car paid off as soon as possible with little or no interest on the initial cost of the vehicle. You should be buying a car for the decade, not for the three year window. Enjoy a nice 4-6 years of not having a car payment to build up funds. This is money that you can stash away in a retirement account, investment account, high-interest online savings account or towards chopping down other debt. 4. Buying the same item over and over again. It is incredible to me that people will buy the same cheap item over and over again. My example is camping chairs. Let's say Chair A is a cheap version that lasts 3 years, but can be bought for $15. What if you could get a better chair (Chair B) for $40 and have it last you 12 years? If you use a chair 100 times a year you would pay about $0.05 per use for Chair A and $0.03 for Chair B. 5. Not having a long-term financial plan and assuming it will all work out. This is a bunch of wishful thinking often by people that spend just as much or more than what came in. Things will eventually work out in the end they say. This isn't the 1970's when pensions were everywhere and you knew you were going to get social security once you hit the eligibility years. We live in a 401K and questionable for social security in 2050 world. With that said you need to be thinking long-term and paying yourself first in the form of first contributing to a retirement account. At the very minimum you should take the maximum company match of your employer, because it is free money. A good goal to have in your retirement account is: By age 30: At least the equivalent of your gross salary By age 35: At least 2x your salary By age 40: 3x Age 45: 4x Age 50: 5x Age 55: 6x Age 60: 7x The most challenge part of this will be the age 30 and 35 years levels. What is good is that you will have compounding interest from your investments working right along with you. It is reasonable to expect an account filled with index funds to have a 6-8% annual growth before you even contribute. Stick to the chart above and you should be able to retire comfortably. Also notice how I didn't say your annual expenses, but your gross salary. Financially responsible people tend to live well below their means, so that pot of money will carry you quite a ways. 6. Taking out loans for liabilities. Boats, vacation homes, diamond rings, vacations, four-wheelers...all have bad return on investments. These items can be fun, but they also tend to be a financial sinkholes. What makes matters worse is taking out a loan to buy them. That just adds lighter fluid to the flame in the form of interest on the principle. As the saying goes, "If you can't afford five of them, you can't buy one of them." 7. Not having an emergency fund. This rings loud particularly now when so many people are out of work. In my particular industry (tourism) the number is around 50% of workers being out of a job. With that said having an emergency fund should be your #1 priority after making sure your most basic bills are paid for. What is recommended is anywhere from 3-6x your monthly expenses. I personally have a nest egg of about six months of expenses. This fund should only be used to cover expenses from lack of income or real emergencies such as medical bills or a fire burning down your house.  This is a subject I get asked about at least a couple times a month in conversation. I keep a really strict budget and still have some funds left over to do some fun activities. I LOVE personal finance blogs, books and videos, so I have taken a lot of nuggets from each source to put together a solid plan. Favorite Blogs: Mr. Money Mustache I Will Teach You to Be Rich Favorite YouTube Channels: Marko - WhiteBoard Finance Minority Mindset Two Cents Favorite Books: I Will Teach You to Be Rich The Millionaire Next Door Rich Dad Poor Dad First off, I keep a detailed monthly budget through Google Sheets. They have a template in-house that you can edit to best fit your lifestyle. Personally, my categories are described as "Needs", "Wants" and Investments. Textbook examples of this call for the 50/30/20 rule where 50% of your post-tax income goes to Needs, 30% to Wants and 20% to Investments. Mine actually breaks down closer to 50/20/30. How I manage my money is very automated, meaning all of my bills are paid for automatically and my investment and high-interest online savings account take money out of my brick-and-mortar bank monthly. Once I've paid those accounts what is left over first must address my needs. Needs (50% Of My Income) Groceries Rent Renter's Insurance Utilities Medical/Dental/Vision (through my employer) Laundry Car Insurance Car Maintenance Gas This list for all intents and purposes is my list of things I need to merely stay alive. My budget for groceries every month is about $200 and I rarely hit that mark. I buy almost exclusively generic brands and cook a lot of large batch meals such as soups. Next on this list is my rent, which is $850/month. This also includes all of my utilities with the exception of plug-in electric, which usually runs about $30/month. This is a pretty good deal in an out-of-whack State College market, where salaries and housing costs make it tough to find housing close to jobs that is less than 30% of your take home pay. Yes, I still use coin operated washers and dryers. It sucks trying to come up with 14 quarters to do a load of laundry in a building that doesn't have a change machine. Lastly, I drive a 2009 Subaru Forester with roughly 111,000 miles on it. The car is completely mine and I have no car payments on it. Growing up near the Great Lakes it is a basic necessity to have All-Wheel Drive. In State College, that isn't as bad where the winters are more mild. In my mind, there is no greater waste of money than buying a fancier luxury automobile or more car than you need, like a F-350 when you haul nothing consistently with it. I live within three miles of my office, so in a given year I only tack on between 8-10K miles. In a typical year, I'm only doing between $500-$700 in car maintenance. This also keeps my gas bill to a minimum. If I was even more ambitious I would ride my bike to work more often. However, I hate getting up early, much less working out within an hour of waking up early. Wants (19%) Cell Phone Haircuts Subscription Services Gym Gifts Charity Shopping/Eating Out Vacation Cell phone as a "Want"? Are you kidding me? Yes. If I lost my cell phone I wouldn't be living on the streets or dying of starvation. My phone is completely paid off and pretty old in the standard of smart phones. I have an iPhone SE, which isn't even given updates by many of the apps we most commonly use. Haircuts used to be a monthly necessity, but COVID-19 gave me the time to teach myself how to cut my own hair. Luckily, I've had a buzz cut for the majority of my life, so that was easy enough. I kindly lack the peacocking need for well maintained hair. Subscription services is rather boring in that I only have Netflix streaming and a membership with the Society of American Baseball Research. Both keep me entertained. My gym is hands down my biggest splurge. I pay $175/month to get group High-Intensity Interval Training (HIIT). I workout at the local F-45 gym in downtown State College. However, I see this investment in my health as more preventative maintenance than anything. Nothing gets between me and my 5:30 PM classes. Gifts and charity are what they are. It is important to give to others and causes that are near and dear. The next item I will break into two categories. When it comes to shopping, I don't tend to do a lot of it. Anyone that knows me is aware of my detest for clutter and rarely used items. I'm not quite a minimalist, but I also live in a 500 square foot apartment, which doesn't allow you to buy a whole lot of junk. I also happen to live right next to a Goodwill, where I get around 50-60% of my clothes. More often than not many of the clothes you buy still have the original sales tag on them. Let someone else pay the steep initial price, but you get the value out of it. Secondly, I probably go out to eat too much. However, this is a perk of living where I do. I can walk to many great restaurants from my front door. State College is pretty underrated when it comes to quality places to eat. As far as vacation goes, this gets decided at the end of the year. Whatever leftovers funds I have from each month go into a pool of funds to go places or buy things I don't really need. In 2019, I ended up with a surplus of about $900. With this money I flew down to Florida to visit my old neighborhood in Cocoa. I also bought a sleeper loveseat to quiet down my friends that visit for Penn State Football and don't want to pay for a hotel. Investments (31%) SEP-IRA (through work) Investment Account High-Interest Online Savings Account Before my money even gets to me, 10% of my gross earnings go to a SEP-IRA account through Merrill Lynch. This contribution level is pretty high, so I wouldn't suggest it for everyone. My employer contributes a 5% equivalent of my salary once a year to this account as well. I had to wait a full year before my employer started to contribute to my retirement fund. Was it a hit to lose that added income? Sure, but you adapt pretty quickly. I intend to pull this percentage back a bit once I hit particular goals in the account. All of the remaining funds from my paycheck go into a traditional brick-and-mortar bank through direct deposit. You know, the ones where you can get lollipops, a safety deposit box and almost dis-locate your wrist when you try to walk away with the latch to the counter pen? Yes, those. Since they don't pay anything in interest, because they seemingly must have an enormous overhead and/or aren't good at making money, I tend to keep the bare minimal amount of funds in this account. What has been recommended to me is keeping the equivalent of one month's worth of expenses. In addition to this, I keep $1,000 in a savings account in the rare occasion I ever overdraw my checking. In 18 years of having this account, this hasn't ever come close to happening. Using the old principle of paying yourself first, 10% of my net income goes to my E-Trade investment platform every month. I didn't pick E-Trade for any particular reason. What happened is I opened an ING Direct account in college, which got bought out by Capital One and then was pawned off onto E-Trade. My personal investment account is the equivalent to a man floating down a lazy river. In that account I buy almost exclusively index funds, because I don't pretend like I am smarter than the market. Another 10% goes to my high-interest online savings account through Barclays. As of writing this I am get a 1.15% interest on this account. This is roughly 12x what I get in my typical brick-and-mortar account. I use this particular account for my emergency fund (totaling 6x your monthly expenses), my new car fund and my house down payment fund. Of note is that every single month I pay my credit card bill in full. I never let my balance move to the next month where I will gain interest. I will sure as heck take their rewards and Cash Back programs though. When people say you should let it carry to build credit history I get a laugh. My FICO score as of this article is a 818, so that is de-bunked. Life is a lot easier when you don't have debt breathing down your neck, so avoid it if at all possible. Things shouldn't cost more than the sticker price. It is always wise to understand and calculate your net worth to see where you stand. To get this number it is simply add up your assets (bank accounts, investment accounts, retirement accounts, car and home values, etc.) and subtract it by your liabilities (debt you have accrued or still owe). According to the book The Millionaire Next Door your number be your age multiplied times your annual salary. For example: Jim makes $40,000 a year and is 31 years of age. His net worth goal should be: $124,000 Through a lot of discipline in my day-to-day life I'm comfortably above my net worth goal, even with a very steep decline in the market this spring. Hopefully that continues and I can keep working towards my next goal of home ownership. Below is a look at my personal income distribution and how it is automated.  |

Archives

September 2020

Categories

All

About the AuthorAndy Rupert is a Penn State (B.A. John Curley Center for Sports Journalism 08') and a Southern Miss (M.S. Sport Management 09'). He has spent his whole career working in sports and tourism digital marketing and metrics. |

||

RSS Feed

RSS Feed